Return to Antravia Advisory

UK VAT for International Businesses

A Practical Compliance Guide - Including Ecommerce & Platform Sellers

Everything non-UK businesses need to know about VAT registration, filing, thresholds, ecommerce marketplace rules, low-value consignments, digital services, and Making Tax Digital (MTD) - in one practical advisory guide from Antravia.

When the United Kingdom left the European Union at the end of 2020, it did not simply exit a trading bloc, but it created an entirely new VAT jurisdiction overnight. Businesses that had relied on EU VAT rules, the Mini One Stop Shop (MOSS), or distance-selling thresholds were suddenly operating in a system with its own registration triggers, its own digital-services regime, its own import mechanics, and its own compliance infrastructure. Failing to recognise that distinction has proven costly for thousands of international businesses.

This guide is structured as two interconnected parts.

The first

UK VAT: A Practical Compliance Guide for International Businesses

covers the foundational rules every cross-border operator must understand: when you must register, how the tax applies to goods versus services, what obligations arise when selling through online marketplaces, how VAT returns work, and what Making Tax Digital (MTD) requires. The second

UK VAT for Ecommerce and Platform Sellers

addresses the specifics that most concern online retailers: low-value consignment rules, deemed supplier provisions, holding stock in the UK, digital services, and import mechanics after Brexit.

Together, these sections are designed to give you, whether you are an overseas manufacturer shipping to British consumers, a SaaS company serving UK subscribers, or a marketplace seller storing inventory in a UK fulfilment centre, a reliable foundation for compliance and commercial planning alike.

Advisory note: UK VAT law is governed principally by the Value Added Tax Act 1994 and secondary legislation. HMRC administers the regime. References to specific rules in this guide reflect the position as at 2025/6. Businesses should always take professional advice tailored to their specific circumstances before acting.

PART ONE: UK VAT — A Practical Compliance Guide for International Businesses

1. Registration Triggers: When Does UK VAT Apply to Your Business?

The most fundamental question for any international business is straightforward: do you need to be registered for UK VAT? The answer depends on what you are supplying, to whom, and from where. There is no single rule that covers every scenario, and therein lies the compliance risk.

1.1 The Standard Threshold

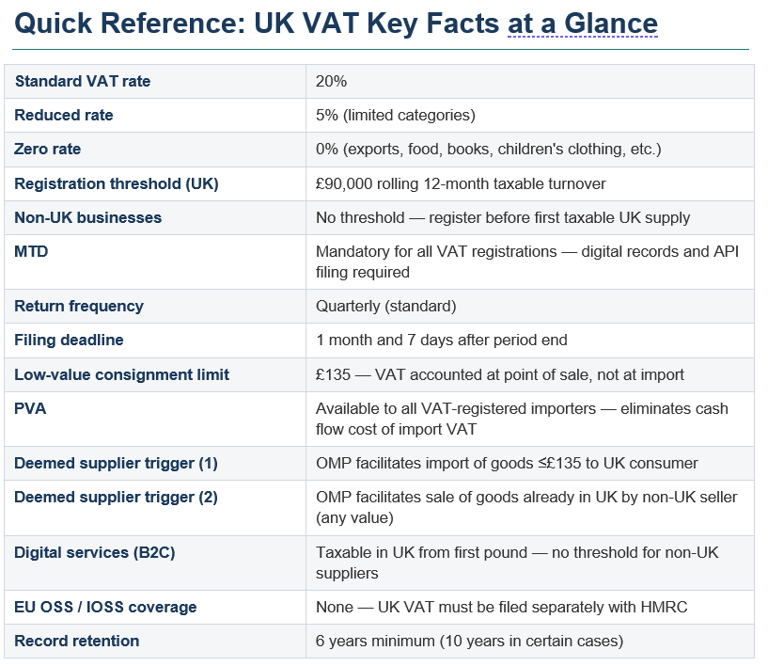

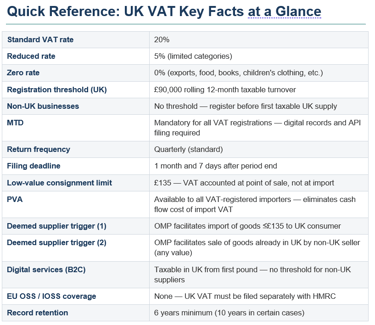

The UK VAT registration threshold is £90,000 of taxable turnover in any rolling 12-month period. This threshold applies to businesses established in the UK, but many non-UK businesses must register without reference to any threshold at all.

Threshold (2025)

£90,000 taxable UK turnover in any rolling 12 months

Registration deadline

30 days after the end of the month you exceeded the threshold

Effective registration

First day of the second month after you exceeded the threshold

Voluntary registration

Allowed at any level of turnover — often commercially advantageous

1.2 Compulsory Registration for Non-UK Businesses — Zero Threshold

If your business is established outside the United Kingdom and you make taxable supplies of goods or services in the UK, you are generally required to register for UK VAT from the very first pound — there is no threshold. This is a critical departure from the EU model and catches many overseas businesses off guard.

The following situations typically trigger an immediate UK VAT registration obligation for a non-UK business:

Supplying goods that are physically located in the UK at the point of sale

Importing goods into the UK and making them available for sale there

Providing digital services to UK consumers (B2C)

Acquiring goods in the UK through intra-UK transactions

Holding goods in a UK fulfilment warehouse (see Part Two)

1.3 The Reverse Charge — When Registration May Not Be Required

Not every supply to a UK business automatically requires the overseas supplier to register. Where a non-UK business supplies services to a UK VAT-registered business, the UK customer typically self-accounts for the tax under the reverse charge mechanism. This shifts the VAT reporting obligation to the customer, relieving the overseas supplier of registration in many B2B service scenarios.

The reverse charge does not apply to supplies of goods, nor does it apply when the customer is a private individual (B2C). Any B2C supply of services that is taxable in the UK falls squarely on the overseas supplier to account for.

1.4 Voluntary Registration

Businesses that fall below the threshold or that would otherwise rely on the reverse charge can still elect to register voluntarily. This is often commercially sensible: it allows recovery of UK input tax on expenses, removes the administrative friction of proving reverse charge eligibility, and signals credibility to UK business customers. Voluntary registrations can also be backdated in limited circumstances with HMRC agreement.

2. Services vs Goods - The Rules That Determine Where VAT Falls

The distinction between goods and services is fundamental to how UK VAT operates across borders. It determines both where a supply is taxed and who is required to account for it. Getting this wrong is one of the most common, and most expensive, errors made by international businesses entering the UK market.

2.1 Supplies of Goods

Goods are tangible, moveable property. For UK VAT purposes, the basic rule is that a supply of goods is taxable in the UK if the goods are in the UK at the time of supply, or if they are imported into the UK as part of the transaction. The rate structure is as follows:

Standard rate (20%)

The default rate applying to most goods and services

Reduced rate (5%)

Applies to specific categories (e.g., children's car seats, energy-saving materials)

Zero rate (0%)

Taxable supply at 0% — most food, children's clothing, books, and exports qualify

Exempt

Outside the scope of VAT — no input tax recovery on related costs

It is important to distinguish between zero-rated and exempt supplies. Both attract no VAT charge to the customer, but zero-rated supplies preserve the right to recover input tax while exempt supplies do not. For international businesses exporting goods from the UK, zero-rating of exports is significant: you charge no VAT to your overseas customer but can recover UK VAT on your related costs.

2.2 Supplies of Services — The Place of Supply Rules

Services do not exist physically, so their 'location' for VAT purposes is determined by specific place-of-supply rules. The general rules are:

B2B services (business to business): taxable where the customer belongs — typically triggering the reverse charge in the customer's country

B2C services (business to consumer): taxable where the supplier belongs — the supplier registers and accounts for VAT in their own jurisdiction

There are numerous exceptions to these general rules, including:

Land-related services: taxable where the land is situated

Event services (admission): taxable where the event takes place

Restaurant and catering services: taxable where physically performed

Passenger transport: taxable where the journey takes place

Digital services supplied B2C: taxable where the consumer is located — see Section 3

Key advisory point: The place-of-supply rules mean that a UK-based business providing digital services to French consumers must consider French VAT, while a US-based business providing those same services to UK consumers must consider UK VAT. The obligations follow the customer's location for most B2C digital supply scenarios.

3. Marketplace Rules — The Deemed Supplier Framework

One of the most transformative changes in UK VAT in recent years is the introduction of deemed supplier rules for online marketplaces. These rules, which came into full effect for UK purposes in 2021, fundamentally shift the VAT liability for a significant portion of ecommerce transactions from the underlying seller to the platform facilitating the sale.

3.1 What the Deemed Supplier Rules Do

Under the deemed supplier framework, an online marketplace (OMP) is treated as if it purchased goods from the underlying seller and then made an onward supply to the final consumer. This means the OMP, and not the seller, accounts for the UK VAT on those transactions. The supply from the underlying seller to the marketplace is treated as a zero-rated or VAT-free business-to-business supply.

The deemed supplier rules apply to an OMP in two core scenarios:

The OMP facilitates the sale of goods imported into the UK in consignments with an intrinsic value not exceeding £135

The OMP facilitates the sale of goods (of any value) by a seller not established in the UK, where those goods are already located in the UK at the point of sale

3.2 What Constitutes an 'Online Marketplace'

HMRC defines an online marketplace broadly. It includes any website, mobile application, or other electronic interface that allows third-party sellers to list goods for sale to UK consumers. Major platforms such as Amazon, eBay, Etsy, and similar marketplaces fall squarely within this definition. The marketplace must 'facilitate' the sale, this meaning it allows customers to place orders with sellers, rather than merely advertising goods.

3.3 Responsibilities that remain with the Seller

Even where the deemed supplier rules apply, underlying sellers retain certain obligations. They remain responsible for accurate product classification and description (which affects VAT rate and import duty), for any VAT on supplies outside the scope of the deemed supplier rules, and for any customs compliance obligations. Sellers should also ensure they provide accurate transaction data to the marketplace, as inaccuracies can expose them to liabilities.

Practical note: If you are a non-UK seller listing goods on a UK-facing marketplace, and those goods are either in the UK or are being imported in consignments under £135, the marketplace will collect and remit the VAT. You should confirm this arrangement with the platform and ensure your pricing, inventory, and invoicing systems reflect it correctly.

4. Filing and Making Tax Digital (MTD) - Your Ongoing Compliance Obligations

Registration is only the beginning. Once your business holds a UK VAT number, you are committed to a cycle of returns, payments, and, increasingly, digital record-keeping. Understanding these obligations before you register, rather than after, avoids penalties and administrative disruption.

4.1 VAT Returns

UK VAT returns are filed quarterly as standard, covering accounting periods aligned with your registration date. Returns must be submitted, and any VAT due paid, within one calendar month and seven days after the end of the relevant period. For a quarterly period ending 31 March, the deadline is 7 May.

Filing frequency

Quarterly (monthly available on application; annual scheme for smaller businesses)

Submission deadline

1 month and 7 days after the end of the VAT period

Payment deadline

Same as submission deadline (usually coincides for electronic payments)

Method

Online via HMRC's VAT online service or compatible MTD software

Currency

All figures in pounds sterling (GBP)

4.2 Making Tax Digital for VAT — MTD

Making Tax Digital (MTD) for VAT is now mandatory for all VAT-registered businesses and without exception for turnover level. MTD requires businesses to:

Maintain digital records of all VAT-relevant transactions

Use MTD-compatible software to submit VAT returns directly to HMRC via an API connection

Preserve a 'digital journey' - data must flow digitally between systems without manual re-entry at any point in the chain

For international businesses, MTD raises particular practical challenges. If your accounting systems are based on non-UK software (SAP, Oracle, NetSuite, QuickBooks in a non-UK configuration, etc.), you will need to ensure that your UK VAT workings can be fed into an MTD-compliant submission tool. Bridging software solutions are available for businesses with legacy or complex ERP environments.

4.3 The VAT Account and Record-Keeping

Businesses must maintain a VAT account so a running record of all output tax charged and input tax claimed. While there is no prescribed format, HMRC requires that records be retained for six years (or 10 years in certain cases). Digital records must include: the time of supply, the value of supply, the VAT rate applied, and the VAT amount. For imported goods, customs documents form part of the VAT record.

4.4 Penalties and the Points System

HMRC operates a points-based late-submission penalty regime for VAT returns. Each missed filing deadline accrues a penalty point. Once points reach the threshold (two points for annual filers, four for quarterly, five for monthly), a fixed £200 penalty applies, with further £200 penalties for each subsequent late submission. Separate penalties apply for late payment, calculated as a percentage of the outstanding amount.

Advisory note for non-UK businesses: HMRC has the power to de-register businesses that fail to file returns or pay VAT. De-registration does not extinguish the underlying tax liability. Businesses that operate informally without registering, or that allow registrations to lapse, face back-assessments, interest, and penalties that can substantially exceed the original tax due.

5. Thresholds — What the Numbers Actually Mean in Practice

The UK VAT threshold landscape can be summarised in a single table, but the practical implications require more careful consideration — particularly for non-UK businesses, where the threshold is effectively zero in most scenarios.

5.1 Summary of Key Thresholds

Standard registration threshold

£90,000 taxable turnover in any rolling 12 months (UK-established businesses)

Non-UK businesses (goods)

£0 — no threshold; registration required from first taxable supply

Non-UK businesses (B2C digital)

£0 — no threshold for digital services to UK consumers

Deregistration threshold

£88,000 — you may deregister if taxable turnover is expected to fall below this

Low-value consignments (goods)

£135 — determines customs and VAT treatment of imported parcels (see Part Two)

Annual accounting scheme upper limit

£1.35 million taxable turnover

Cash accounting scheme upper limit

£1.35 million taxable turnover

Flat rate scheme upper limit

£150,000 VAT-exclusive turnover

5.2 How the Rolling 12-Month Test Works

The threshold is not assessed on a calendar-year or financial-year basis. At the end of every calendar month, you must look back at the previous 12 months of taxable turnover. If that cumulative figure exceeds £90,000, you have a registration obligation. The obligation arises even if you expect turnover to fall, a forward-looking exemption is only available in limited, specific circumstances where you can demonstrate to HMRC that the breach was a one-off.

For non-UK businesses selling goods that are already in the UK, or providing B2C digital services, the rolling 12-month test is largely irrelevant: the obligation to register arises before any threshold is reached. The threshold is primarily protective for UK-established businesses and for overseas businesses with genuinely minimal UK activity.

5.3 Threshold Planning — Practical Considerations

For businesses operating close to the threshold, voluntary early registration offers a clean start and avoids the risk of a retrospective assessment. Businesses that register late, after exceeding the threshold, remain liable for VAT on all sales from the date registration should have begun, not from the date they actually registered. This can create a significant liability, particularly where prices were set exclusive of VAT and retrospective recovery from customers is impossible.

PART TWO: UK VAT for Ecommerce and Platform Sellers

The rules governing ecommerce VAT in the UK are, in practical terms, some of the most consequential in the entire regime. Since 2021, the UK has operated a post-Brexit framework specifically designed for cross-border online sales, replacing the EU distance-selling model that ceased to apply at the end of the transition period. This section addresses the rules that matter most to online retailers, platform operators, and digital service providers.

6. Low-Value Consignments — The £135 Rule and its Implications

Prior to January 2021, goods imported into the UK in consignments valued at or below £15 were exempt from import VAT. This created a well-documented arbitrage that allowed overseas retailers to undercut UK-based competitors by avoiding VAT on small shipments. The UK eliminated this relief as part of its post-Brexit VAT reform, replacing it with an entirely new framework.

6.1 How the £135 Threshold Works

For goods imported into the UK in consignments with an intrinsic value not exceeding £135, import VAT is not collected at the border. Instead, VAT is accounted for at the point of sale, by either the seller or the online marketplace facilitating the transaction. The '£135' refers to the intrinsic value of the goods — the customs value excluding transport, insurance, and any separately stated taxes or duties.

Consignment value ≤ £135

VAT accounted for at point of sale, not at import

Seller VAT obligation

Overseas seller must register and charge UK VAT on sale to UK consumer

Marketplace obligation

If sold via an OMP, the marketplace accounts for the VAT as deemed supplier

Customer type

Applies to B2C sales; B2B sales may use reverse charge instead

Consignment over £135

Import VAT collected at the UK border by HMRC; standard customs procedures apply

6.2 What This Means for Direct-to-Consumer Sellers

If you are a business outside the UK shipping individual parcels directly to UK consumers, and the value of each parcel is £135 or below, you are required to:

Register for UK VAT

Charge UK VAT (at the applicable rate) on each sale to a UK consumer

File UK VAT returns and remit the tax collected to HMRC

The customs declaration for such goods must indicate that the VAT has been accounted for at the point of sale. HMRC has produced specific customs procedure codes for this purpose. Failing to handle this correctly can result in VAT being collected twice, once by the seller and once at the border, which creates refund complexity and customer service problems.

6.3 Excise Goods and Consignment Splitting

The £135 threshold does not apply to excise goods (such as alcohol and tobacco), which always attract import duty and VAT at the border regardless of value. It also does not apply to goods subject to anti-dumping duties or countervailing charges.

HMRC is vigilant about consignment splitting, artificially breaking up larger orders into multiple sub-£135 parcels to remain within the threshold. Where HMRC determines that goods are part of a larger commercial transaction that has been artificially divided, it may aggregate the values for customs and VAT purposes.

Advisory note: The £135 threshold applies to the intrinsic value of goods in a single consignment, not the total value of an order. However, if a single customer order is artificially split into multiple consignments purely to remain under the threshold, HMRC has the power to disregard that artificial structure. Businesses should document the commercial rationale for any multi-parcel shipping arrangement.

7. Marketplace Deemed Supplier Rules in Practice

The deemed supplier rules introduced in 2021 represent the single most significant structural change to UK ecommerce VAT in the post-Brexit era. While Section 3 provided an overview of the framework, this section addresses how those rules operate at the level of day-to-day commercial activity.

7.1 The Two Pathways to Deemed Supplier Status

An online marketplace becomes a deemed supplier in two distinct scenarios, each with different implications:

Pathway A — Imported Goods (£135 or under): When an OMP facilitates the sale of goods imported into the UK from outside, and the consignment value does not exceed £135, the OMP is deemed to have made the supply to the UK consumer. It charges and collects UK VAT from the consumer and accounts for it to HMRC. The underlying seller makes a deemed B2B supply to the OMP at zero rate.

Pathway B — Goods Already in the UK (Non-UK Seller, Any Value): Where a non-UK established seller lists goods that are already physically located in the UK — in a fulfilment centre, a third-party warehouse, or any other UK location and the OMP facilitating the sale is the deemed supplier regardless of the consignment value. A non-UK seller with £500 goods stored in a UK warehouse and sold via an OMP will see the OMP account for the VAT.

7.2 Implications for UK-Established Sellers

The deemed supplier rules apply specifically to non-UK established sellers. A seller that is established in the UK and sells through a marketplace remains responsible for its own VAT accounting. The marketplace does not become the deemed supplier for UK-established sellers in most circumstances. This distinction matters enormously if your business is considering whether to establish a UK entity, as doing so shifts the VAT responsibility away from the platform.

7.3 Seller Obligations in a Deemed Supplier Transaction

Even where a marketplace is the deemed supplier, the underlying seller has obligations:

Provide the marketplace with accurate commodity codes, descriptions, and valuations

Ensure the goods comply with UK customs and trade regulations

Account for any VAT on supplies falling outside the deemed supplier scope (e.g., B2B sales where the buyer provides a UK VAT number)

Register for UK VAT independently if the business makes any UK supplies outside the marketplace context

Practical implication: Many cross-border sellers assume that because a marketplace handles the VAT on their UK sales, they have no UK VAT obligation at all. This is not always correct. If you sell direct-to-consumer outside the marketplace, via your own website, for instance, those direct sales are entirely your own responsibility.

8. Digital Services - VAT on Electronically Supplied Services

The UK maintains its own regime for the VAT treatment of electronically supplied services (ESS) to consumers, one that pre-dates Brexit and has been retained and updated in the post-EU environment. For SaaS companies, streaming platforms, app stores, digital publishers, and similar businesses, this regime is essential reading.

8.1 What Counts as a Digital Service

HMRC defines digital services broadly as services delivered over the internet or an electronic network, automatically, with minimal human involvement. Examples include:

Software, applications, and games (including in-app purchases)

Music, video, and podcast streaming or download services

E-books, digital newspapers, and online publications

Web hosting, domain registration, and cloud storage

Online courses and educational content delivered automatically

Online marketplaces and platforms (in their service capacity to sellers)

Services that require substantial human involvement, such as bespoke online training, legal advice delivered by email, or custom software development, are generally not treated as digital services and fall under the general B2B or B2C service rules instead.

8.2 The UK Taxation Point for Digital Services

For B2C digital services supplied to UK consumers, VAT is chargeable in the UK regardless of where the supplier is established. A US software company, a Singapore streaming platform, a German app developer, all are required to register for UK VAT and charge UK VAT on sales to UK consumers. There is no turnover threshold below which this obligation can be avoided.

8.3 Determining the Consumer's Location

Because the obligation depends on where the consumer is located, suppliers must take reasonable steps to determine that location. HMRC permits a rebuttable presumption based on two non-contradictory pieces of evidence, which can include:

The billing address of the customer

The internet protocol (IP) address of the device used

The billing address associated with the payment method

The country code of the SIM card used

The location of the fixed landline through which the service is supplied

Where the evidence points in contradictory directions, suppliers must use their best judgment and document the decision. Businesses processing large volumes of transactions should have automated location-determination logic embedded in their checkout and billing systems.

8.4 No Separate Non-Union MOSS for the UK

The EU's One Stop Shop (OSS) and Import One Stop Shop (IOSS) regimes, which allow businesses to file a single EU-wide return for digital services and imported goods respectively, do not extend to the UK. There is no equivalent 'UK MOSS' or 'UK IOSS' for non-UK businesses. Businesses supplying digital services to both UK and EU consumers must handle their UK VAT obligations completely separately from their EU obligations, filing separate returns in each jurisdiction.

Advisory note: If your business currently files an EU OSS or IOSS return covering sales to European consumers, that return covers nothing in respect of your UK obligations. UK VAT must be reported to HMRC directly through a UK VAT registration. Many businesses overlook this duplication of obligations after Brexit.

9. Holding UK Stock - Fulfilment Centres, Warehouses, and Fixed Establishments

The decision to hold stock in the United Kingdom, whether in your own warehouse, a third-party logistics provider, or an Amazon Fulfilment by Amazon (FBA) centre, is one of the most commercially significant VAT triggers for international sellers. Understanding the consequences before you make that operational decision is essential.

9.1 Why Stock in the UK Creates a VAT Obligation

When goods are physically located in the UK and available for sale to UK customers, those goods are 'in the UK' for VAT purposes. A sale of those goods is a UK supply. If you are not UK-established, there is no threshold, you must register for UK VAT before making any such sales.

The mere act of sending stock to the UK, even before any sale is made, is often treated as either an import (subject to UK customs and import VAT procedures) or a transfer of own goods. Either way, it creates a VAT presence that requires registration.

9.2 Amazon FBA and Similar Platforms

Sellers using Amazon FBA or similar fulfilment programmes are required to register for UK VAT independently of any obligations that Amazon itself may have as a marketplace. Amazon does not register on your behalf. When your inventory enters an Amazon UK fulfilment centre:

You are importing goods into the UK, import VAT and potentially customs duty are payable

The goods are now in the UK, which means any sale from that inventory is a UK supply

If you are non-UK established, Amazon becomes the deemed supplier for your consumer sales, but you remain responsible for the import VAT on the initial inbound shipment

9.3 Fixed Establishment Risk

The concept of a fixed establishment is important to monitor carefully. HMRC may take the view that a non-UK business that holds stock in the UK, employs UK staff, or has a UK agent acting in its name on a habitual basis has a fixed establishment in the UK. This can affect the place of supply of services, the applicability of the reverse charge, and ultimately your overall UK tax position. The presence of significant UK physical infrastructure, warehousing, logistics, customer service operations, deserves specific professional analysis.

Practical note: Before placing stock in a UK fulfilment centre, ensure you have a UK VAT number and an EORI (Economic Operators Registration and Identification) number for customs purposes. The cost of import VAT is often recoverable through your VAT return, but only if you are registered and have obtained the correct customs documentation (C79 certificate for standard imports, or the relevant postponed import VAT statement for PVA).

10. Import Mechanics - How UK Customs and VAT Interact

Post-Brexit, every movement of goods from outside the UK into the UK is an import, including shipments from the EU, which were previously free-movement intra-Community transactions. Understanding how customs duty, import VAT, and the various customs procedures interact is essential for any business shipping goods to UK customers or UK fulfilment locations.

10.1 The Import VAT Framework

When goods are imported into the UK, import VAT is payable at the standard rate applicable to those goods (typically 20%). Import VAT is calculated on the customs value of the goods, broadly, the transaction value, plus any applicable customs duty, freight, and insurance costs (the 'CIF' basis for customs value purposes).

For VAT-registered businesses, import VAT is recoverable as input tax, subject to the normal rules. This recovery is evidenced by the C79 certificate issued by HMRC monthly for VAT-registered importers, or alternatively through Postponed VAT Accounting statements.

10.2 Postponed VAT Accounting (PVA)

Postponed VAT Accounting is the UK's mechanism for allowing VAT-registered businesses to defer import VAT from the point of import to their next VAT return. Rather than paying import VAT upfront at the border, which creates a cash flow cost that must then be reclaimed on the quarterly return, businesses can account for import VAT on the VAT return itself. The output VAT charge and the input VAT recovery appear in the same return period, effectively eliminating the cash flow cost.

Eligibility

Any VAT-registered importer with a UK EORI number

How to use

Declare PVA on the customs declaration (procedure code C1 or equivalent)

Evidence for recovery

Monthly postponed import VAT statement (downloaded from HMRC online account)

Cash flow benefit

No upfront import VAT payment — accounted for on VAT return

Key risk

Must ensure statements are downloaded and retained as evidence for recovery

10.3 Customs Duty Considerations

Import VAT is separate from, and in addition to, any applicable customs duty. Customs duty rates are set by the UK Global Tariff (UKGT) and vary by commodity code. Unlike import VAT, customs duty is generally not recoverable, it is a cost of import that either the seller or the buyer bears depending on the agreed Incoterm. For consumer goods shipped B2C under the delivered-duty-paid (DDP) Incoterm, the seller bears the customs duty, which must be factored into pricing.

10.4 Incoterms and Customer Experience

The choice of Incoterm has direct consequences for how UK customs charges are handled. Under DDP (Delivered Duty Paid), all taxes and duties are the seller's responsibility, the customer receives their goods without any additional charges at the door. Under DAP (Delivered at Place) or DDU (Delivered Duty Unpaid), the customer is responsible for paying customs duty and import VAT upon delivery, which frequently leads to poor customer experience, parcel abandonment, and returns.

For consumer-facing brands selling into the UK, DDP is strongly recommended from both a commercial and a compliance perspective. It ensures the seller controls the VAT and customs process, avoids unexpected customer charges, and reduces the risk of goods being returned or stuck at customs.

Conclusion: Building a UK VAT-Compliant Structure

UK VAT is a mature, technically detailed regime that has evolved significantly since the end of the Brexit transition period. For international businesses, the combination of no-threshold registration obligations, mandatory digital filing under MTD, transformed marketplace rules, and a standalone import VAT framework creates a compliance environment that demands deliberate planning rather than reactive response.

The businesses that manage UK VAT well share certain characteristics. They establish VAT registration before they need it, not after a threshold breach triggers a retrospective assessment. They integrate UK VAT into their pricing, invoicing, and ERP systems from day one rather than treating it as an afterthought. They understand whether their marketplace obligations are being handled by the platform or by them directly, and they have confirmed that understanding in writing with the platform. And they treat MTD as an infrastructure requirement, not a filing formality.

At Antravia Advisory, we work with international businesses at every stage of their UK VAT journey, from initial registration and compliance structuring through to complex disputes and restructuring. Whether your primary question is whether you need to register, how to handle FBA stock, or how to navigate an HMRC enquiry, our team is available to provide the specific, practical advice your business needs.

To discuss your UK VAT position with the Antravia Advisory team, please get in touch via our website or contact your dedicated advisor directly. This guide is provided for informational purposes and does not constitute legal or tax advice specific to your circumstances.

References

GOV.UK VAT rates: https://www.gov.uk/vat-rates

VAT thresholds: https://www.gov.uk/how-vat-works/vat-thresholds

Imports and PVA: https://www.gov.uk/guidance/check-when-you-can-account-for-import-vat-on-your-vat-return

Overseas sellers/digital: https://www.gov.uk/guidance/vat-on-goods-sold-directly-to-customers-in-the-uk-by-overseas-sellers

Not sure where to start? Antravia U.K. free Consultation

Disclaimer:

Content published by Antravia is provided for informational purposes only and reflects research, industry analysis, and our professional perspective. It does not constitute legal, tax, or accounting advice. Regulations vary by jurisdiction, and individual circumstances differ. Readers should seek advice from a qualified professional before making decisions that could affect their business.

See also our Disclaimer page

Antravia Advisory

Where Travel Meets Smart Finance

Not legal advice, always verify with your Accountant

Email:

Contact us:

Antravia LLC

© 2025. All rights reserved. | Disclaimer | Privacy Policy | Terms of Use |

© 2025 UKVAT.tax — part of the Antravia Group.

Antravia.com | Antravia.co.uk | Antravia.ae |

Finance.travel | Tax.travel | Consultancy.travel | VAT.travel | VAT.claims |

USSales.tax | EuroVAT.tax | UKVAT.tax |

contact@antravia.com

Antravia LLC

4539 N 22nd St., Ste. N

Phoenix

Arizona

85016